Creating a lasting legacy is more than just distributing wealth, it is about preserving values, securing futures, and leaving behind a meaningful impact. Whether it involves financial assets, cherished heirlooms, or philanthropic contributions, legacy planning allows individuals to shape how they are remembered and ensure that their intentions are respected. A detailed legacy plan must address legal, financial, and emotional factors.

Legal & Financial Aspects are Key

Effective legacy planning begins with a clear understanding of the legal and financial frameworks that govern asset distribution. These aspects ensure that an estate is handled according to the individual’s wishes while minimizing potential conflicts, delays, and tax liabilities. At the heart of any legacy planning is the preparation of a legal document which is either a will or a trust.

While a Will serves as a foundational document for the distribution of assets upon death, a Trust can be a valuable tool, especially for individuals who have more extensive estate and specific wishes. Trusts also bypass the probate process required of a Will, ensuring a faster and more private distribution of assets. They also offer greater flexibility, such as allowing for staggered distributions to beneficiaries or setting conditions for inheritance. Furthermore, Trusts can help reduce estate taxes and protect assets from legal challenges. According to private wealth management company Areca Capital Sdn Bhd, a Trust is usually set up for the long term – beyond the lifetime of the settlor for the benefit of the family as beneficiary.

“The biggest misconception among Malaysians about Trust is that such instrument is only reserved for the ultra-high-net-worth individuals. As a private wealth management company established since 2006, Areca Capital has been helping our clients set up Family Trusts with assets from RM1 million onwards,” said Danny Wong, CEO and Executive Director of Areca Capital.

A Trust encompasses a much more comprehensive and specific distribution plan versus a Will. It can be activated during or after a person’s lifetime, whereas a Will only takes effect upon a person’s demise. However, finalising the distribution plan of a Private Trust takes requires a longer timeframe as compared to a basic Will. One of the biggest challenges in setting up a Trust is also the financial and time costs involved. Moving costs of Trust assets, such as stamp duty, legal fees and other expenses need to be taken into account.

“Another common pitfall is underestimating the effects of Trust assets’ sustainability to meet its objectives. This usually happens when insufficient consideration was given to the future inflation and costs for the Trust distribution, such as medical and living expenses. This depletes the Trust assets faster than anticipated,” added Wong.

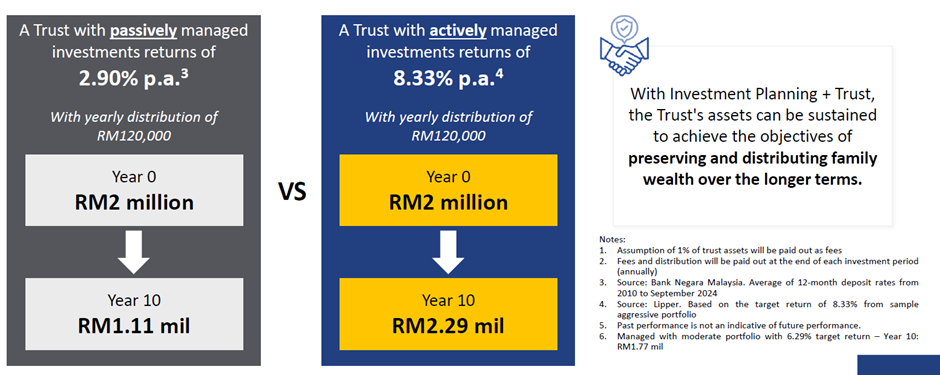

Assume a certain amount of Trust assets is expected to last over 30 years but is passively managed. Inflation and costs could deplete the asset value sooner than expected. Therefore, both estate planning and investment planning are critical for a long-term trust. The impact of a well-managed investment portion of the Trust assets can go a long way.

Estate taxes, inheritance taxes, and other financial obligations can also significantly reduce the value of what is passed on to heirs. Strategic tax planning is therefore needed to minimize this impact. For example, gifting assets during one’s lifetime can reduce the taxable estate. Individuals can also gift up to a certain amount each year, thereby transferring wealth gradually and avoiding significant tax liabilities. Similarly, life insurance policies can play a dual role in legacy planning by providing financial security to loved ones and covering estate taxes or debts to ensure that beneficiaries receive the full intended value of the estate.

Selecting a Legacy Planner

Selecting the right planner ensures that every aspect of the legacy aligns with personal values, financial goals, and legal requirements. Legacy planners often combine expertise in financial planning, legal advisory, and wealth management. They assess the scope and value of an estate, draft legal documents such as wills and trusts, provide tax planning strategies, and advise on asset management and distribution. In a nutshell, a legacy planner serves as a trusted advisor, guiding individuals through the complexities of planning for future generations.

When choosing a trustee company to set up and manage a Trust, consider its reputation, establishment duration, and financial background, especially if it is linked to banking corporations or licensed fund management companies. “Clients who want active management of their Trust assets should take into account a trustee with ties to an investment house or fund manager. This allows for effective estate planning and asset management, ensuring assets are distributed as intended and sustained to meet their goals,” advised Wong.

In recent years, Areca Capital has received increasing enquiries about wealth transfer. Recognizing this need, the private wealth management company acquired Alliance Trustee Berhad in 2023, renaming it Areca Capital Trustees Berhad.

“This acquisition allows us to offer a unified wealth platform, combining investment and trust planning for seamless and sustainable legacy planning, helping our clients achieve their distribution goals during and after their lifetime,” Wong explained.

Legacy Planning: An Evolving Undertaking

Legacy planning should not be viewed as a static, one-time task. It is crucial to regularly review and update the plan, particularly after significant life events. This ensures that one’s legacy remains aligned with personal wishes and current circumstances, safeguarding intentions and providing peace of mind for both the individual and their loved ones. Engaging in thoughtful and proactive legacy planning today can secure a lasting impact that truly reflects one’s core principles and values.

A Smart & Prudent Legacy for the Future is the third and final part in BizTech Times’ editorial series on Legacy Planning.